Additives can decide whether lubricant plants run smoothly or stop. In the Middle East, recent market data shows why the “additives bottleneck” matters. IndexBox reports that the Middle East market for prepared additives for mineral oils contracted in 2024, with consumption falling to 225K tons (valued at $862M). This followed a 2023 volume peak of 306K tons and a 2023 value peak of $1.2B. These swings are a supply-risk signal for the lubricant additives supply chain.

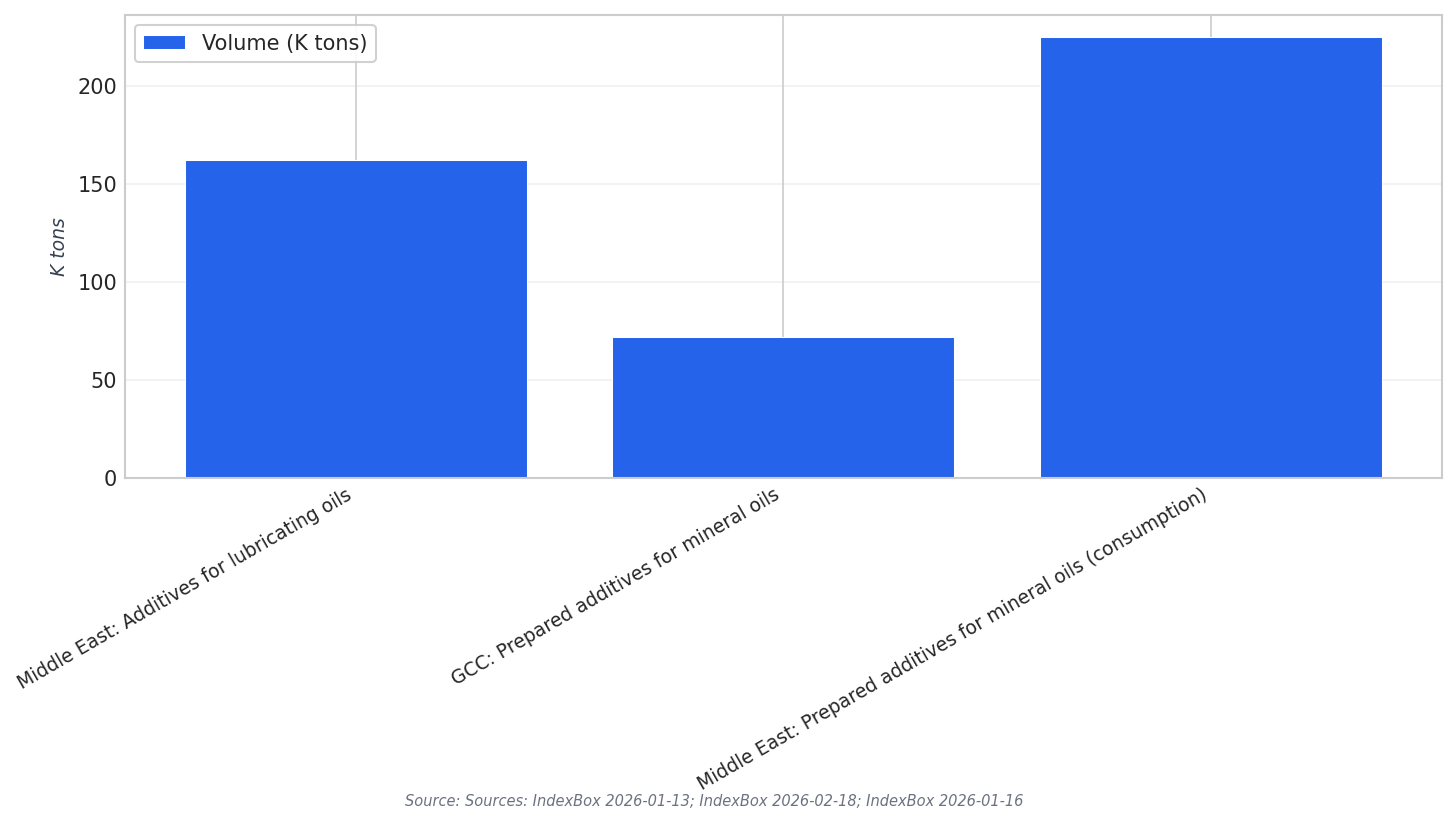

The same pattern appears in additives for lubricating oils. IndexBox reports that Middle East consumption fell by -20.6% in 2024 to 328K tons, while market value declined to $1.3B. Consumption had peaked at 422K tons in 2022, and value had hit $1.6B in 2022. When demand shifts this sharply, procurement plans, inventory levels, and supplier commitments can become misaligned.

Risk rises when imports tighten. For additives for lubricating oils, IndexBox notes the region is a net importer and says imports declined sharply in 2024 to 162K tons, while exports are minimal and concentrated in the UAE. In the GCC prepared additives for mineral oils segment, IndexBox reports supplies from abroad decreased by -63.5% in 2024 to 72K tons. A lubricant blender that depends on imports faces both availability risk and lead-time risk when volumes drop this hard.

Where the Bottleneck Concentrates in the Middle East

Concentration by country can amplify additive supply risk. In prepared additives for mineral oils, IndexBox lists the largest 2024 consumers as Turkey (63K tons), the UAE (49K tons), and Saudi Arabia (43K tons), together comprising 69% of total consumption. For additives for lubricating oils, IndexBox reports Turkey dominates, accounting for 65% of consumption and 90% of production. This concentration can shape bargaining power, priority allocations, and exposure for smaller markets.

Some additive chemistries have their own constraints. In lubricant antioxidants, IndexBox estimates a 2026 Middle East market of approximately USD 180–220 million and states that over 70% of consumption is met through imports, with Saudi Arabia and the UAE as primary import hubs and blending centers. The same report lists bottlenecks like specialty phenol/amine feedstock availability and pricing, high-purity phosphorus derivatives supply, multi-step synthesis capacity for complex molecules, regulatory certification timelines for new chemistries, and IP restrictions on high-performance molecule production. It also notes certification timelines can delay product launches by 12–24 months.

Mitigation starts with planning around what the data shows: import dependence, hub concentration, and volatility. IndexBox forecasts also imply the bottleneck will matter for years. Prepared additives for mineral oils are projected to reach 276K tons and $1.2B by 2035. Additives for lubricating oils are projected to reach 404K tons and $1.7B by 2035. If demand rebounds while import and certification constraints persist, resilience in the lubricant additives supply chain becomes a core operating requirement for Middle East lubricant producers.

Why is the lubricant additives supply chain a bottleneck in Middle East lubricant production?

Which countries dominate prepared additives for mineral oils consumption in 2024?

What happened to Middle East imports of additives for lubricating oils in 2024?

How import-reliant is the Middle East lubricant antioxidants segment?

What non-price constraints can delay new additive adoption in the region?