Shipping activity is a core demand lever for marine lubricants. Multiple market sources link lubricant consumption to rising global shipping volumes, expanding maritime trade routes, and higher vessel operations. These operating hours drive use across engine oils, hydraulic fluids, compressor oils, and other onboard lubrication needs.

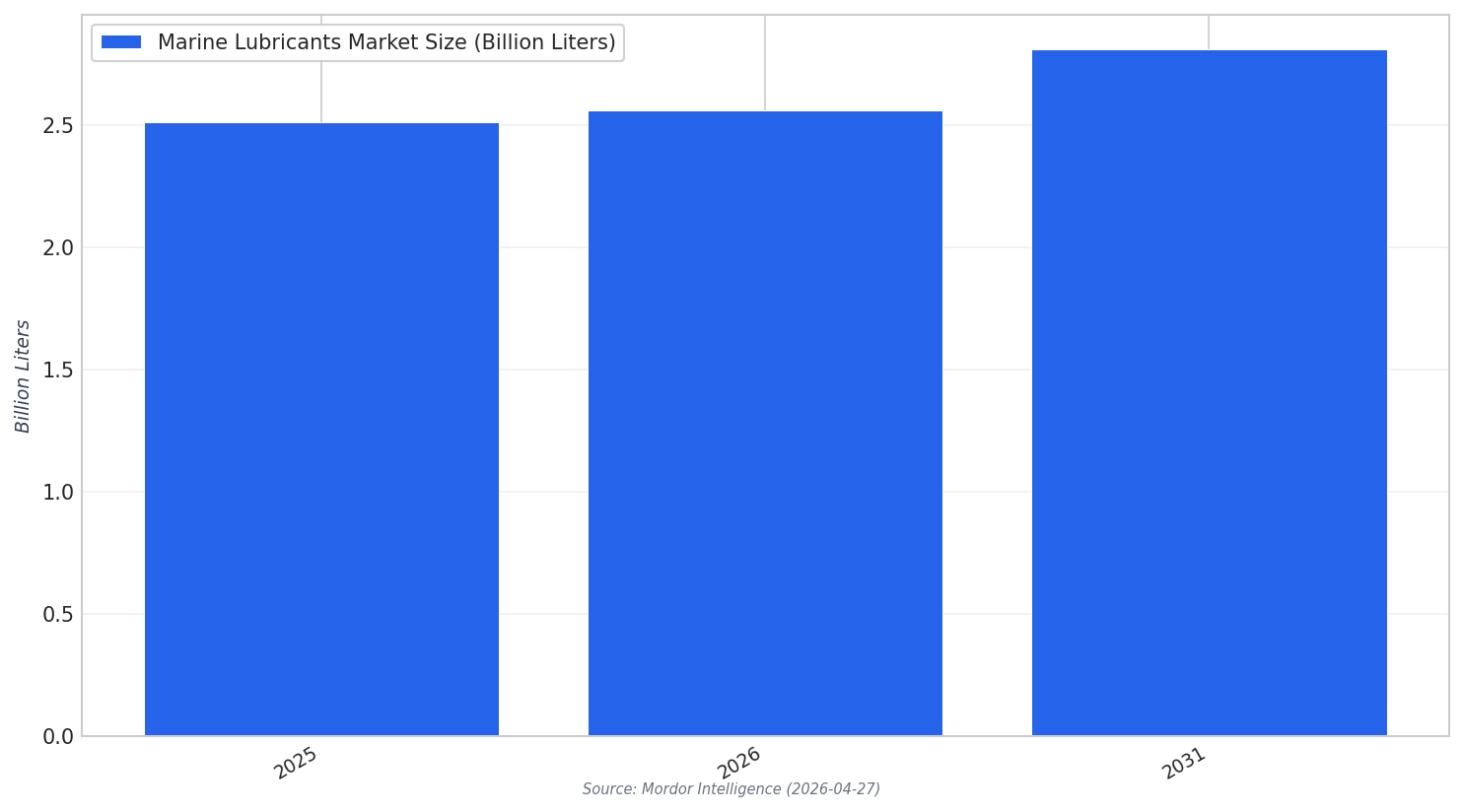

Globally, the market is expected to expand in both value and volume. Market.us projects the global marine lubricants market at USD 8.1 billion in 2025, rising to USD 10.8 billion by 2035, at a 2.9% CAGR from 2026 to 2035. Mordor Intelligence estimates 2.51 billion liters in 2025, increasing to 2.56 billion liters in 2026 and reaching 2.81 billion liters by 2031, at a 1.92% CAGR for 2026-2031.

For marine lubricants demand GCC, the practical mechanism is straightforward. More trade-lane throughput and more port activity tend to mean more voyages, more maneuvering, and more time at load. That raises maintenance needs and lubricant consumption across propulsion and auxiliary systems, even as fleets seek better performance and longer drain intervals.

Why More Port Calls Translate Into Higher Lubricant Pull

Demand growth also reflects what is being lubricated and where consumption concentrates. Mordor Intelligence reports main propulsion captured 52.21% of 2025 volume. It also notes trunk-piston engine oil led with 41.92% of 2025 volume. By ship type, bulkers held 57.14% of 2025 demand, while offshore support vessels show the highest projected CAGR at 2.13% through 2031.

Regulatory and technology shifts are reshaping product mix. Mordor Intelligence states that as the IMO-2020 sulfur cap continues to be enforced, demand is increasingly shifting toward premium 40-BN cylinder oils. It also highlights movement toward synthetic and bio-based grades in areas such as offshore wind vessels and dynamic-positioned support vessels. MarketResearchFuture adds that the expansion of maritime transportation necessitates reliable and efficient lubricants, and cites industry estimates that adoption of advanced lubricants can result in fuel savings of up to 5-10%.

Supply patterns matter as lane and port activity increases. Mordor Intelligence reports direct supply held 66.22% of 2025 volume, while online platforms are the fastest-growing channel at a 2.35% CAGR through 2031. Meanwhile, Market.us expects continued growth supported by rising global shipping activity and modernization of fleets. Together, these dynamics help explain why marine lubricants demand GCC can lift alongside busier shipping lanes and expanding port operations, even when the cited market figures are global rather than GCC-specific.

What is the main link between busier shipping lanes and lubricant demand?

What do forecasts say about overall market growth?

Which onboard area accounts for the largest share of lubricant volume?

How does IMO-2020 influence lubricant choices?

How does this relate to marine lubricants demand GCC?