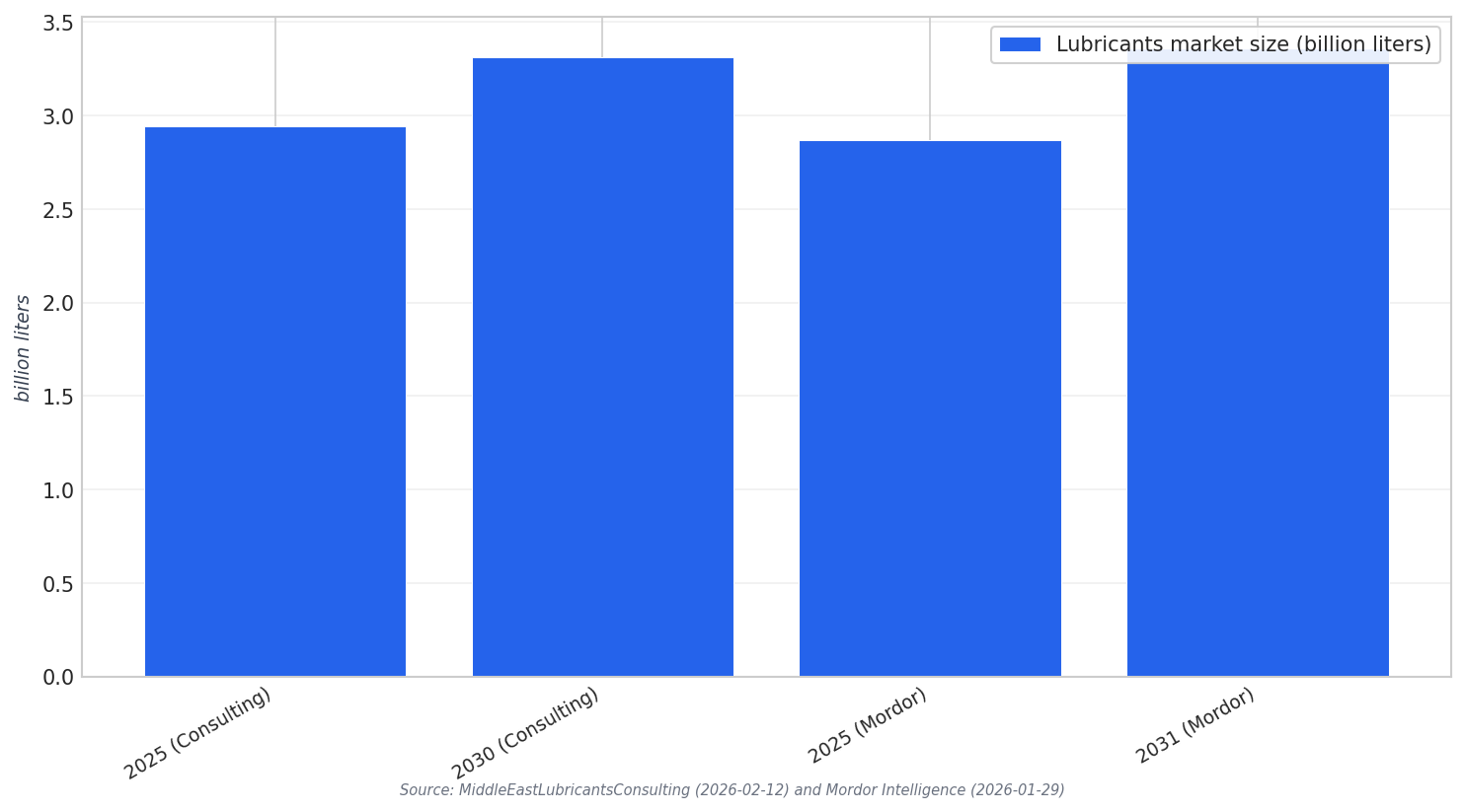

Fragmented routes to market define the region. Yet volume fundamentals are moving in one direction. One outlook projects the Middle East lubricants market growing from 2.94 billion liters in 2025 to 3.31 billion liters by 2030, a 2.43% CAGR. Another estimates 2.87 billion liters in 2025, rising to 3.36 billion liters by 2031 at a 2.66% CAGR. These ranges matter for a lubricant distribution strategy Middle East leaders can scale without overbuilding inventory.

The demand base is not uniform. Automotive and other transportation commanded 45.02% of the Middle East lubricants market size in 2025. Engine oils held 37.32% revenue share in 2025. Industrial pull is also strong as Gulf diversification agendas expand metals, cement, power generation, and manufacturing, while oil and gas keeps consuming high-performance lubricants for exploration, refining, and petrochemicals.

Market concentration also shapes distribution design. Saudi Arabia led with 37.21% of the Middle East lubricants market share in 2025. The UAE is the fastest-growing geography at a 3.21% CAGR through 2031. In Saudi Arabia, internal combustion engine vehicles are projected to remain dominant for the next 15–20 years, supporting steady lubricant demand even as EV adoption grows.

How to Build a Distribution Blueprint That Survives Fragmentation

Start with country-by-country channel realities and then standardize what you can. In Saudi Arabia, a case study shows the value of collaborating with local partners to build a scalable network that reaches urban, industrial, and remote areas. It also highlights training modules for distributors and retailers to keep technical messaging consistent. That same work emphasized localized product offerings, including formulations designed for high-temperature resistance.

Then align portfolio and service depth to where growth is shifting. Group I held 46.62% share in 2025, while Group III is projected to expand at a 2.97% CAGR through 2031. Mineral oils accounted for 69.58% share in 2025, while bio-based lubricants are forecast to grow at a 3.12% CAGR to 2031. Transmission and hydraulic fluids are advancing at a 3.01% CAGR between 2026–2031, and power generation is the fastest end-user at a 3.09% CAGR to 2031. IndexBox also flags intensifying competition beyond price, with value-added services like lubrication management and condition monitoring becoming differentiators.

Finally, design distribution around speed, compliance, and modern buying behavior. Mordor notes that suppliers localizing blending and packaging under 70% iktva content rules can gain price and lead-time advantages, encouraging capacity additions in Yanbu, Jebel Ali, and Sohar. Another Saudi-focused source adds that distribution is being revolutionized by mix-and-match facilities, brand collaborations, and internet platforms. Put together, a practical lubricant distribution strategy Middle East operators can execute is hybrid: localized supply where rules reward it, partner-led coverage for remote demand, and digitally enabled replenishment for fast-moving channels.

What does “lubricant distribution strategy Middle East” mean in practice?

Why does Saudi Arabia matter so much for distribution planning?

Which end-use segments are shaping channel priorities?

What product mix shifts should distributors plan for?

What operational moves improve availability and consistency?