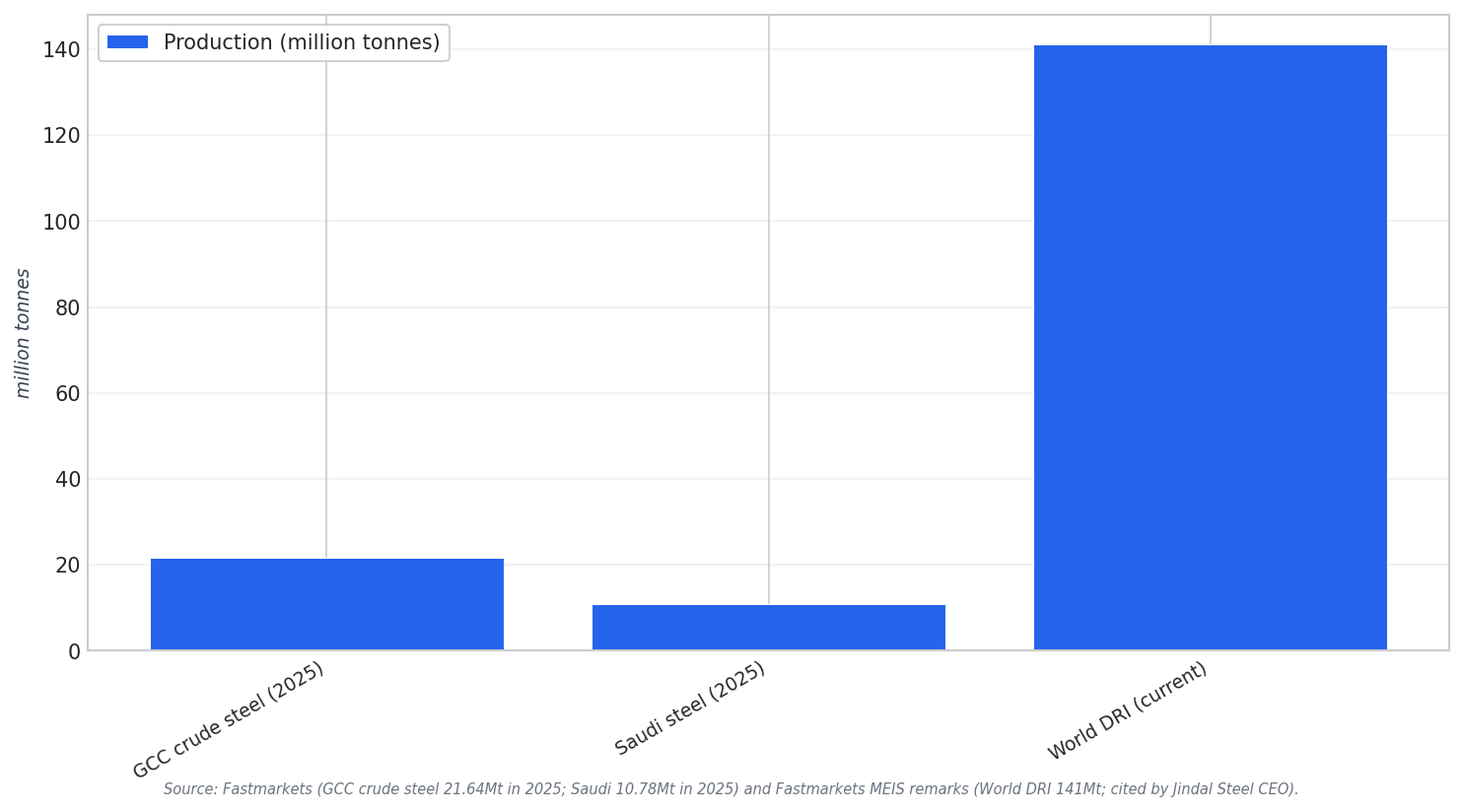

In the GCC, steel production and demand signals are changing fast, and steel mill lubricants GCC plants rely on sit in the middle of that operational pressure. GCC crude steel production hit 21.64 million tonnes in 2025, up by 9.5% year on year, according to the Arab Iron and Steel Union (AISU). Saudi Arabia produced 10.78 million tonnes of steel alone, an increase of 12.3% year on year. At the same time, mills have faced disruptions. Fastmarkets reported that deliveries of key inputs such as iron ore pellets and ferroalloys into the Gulf were disrupted by the blockage of the Strait of Hormuz over five weeks, forcing some cutbacks.

Reheat furnaces set the tone for downstream performance, and lubrication planning often starts with how heat is generated and controlled. Trymax Furnaces describes billet reheating furnace heating zones that raise billet temperature to rolling or forging levels, often above 1,100°C, followed by a soaking zone to drive uniform heat into the core. Temperature monitoring uses advanced sensors and automated controls to prevent hotspots or overheating. Another reheat-furnace reference from Steel Technology notes that patented burners can be designed to provide uniform billet heating, minimize scale formation, and reduce fuel consumption and pollutant emissions. The same source links this to improved billet temperature consistency and enhanced rolling performance.

Rolling Mills, DRI-EAF Reality, and What Changes in the Lubrication Conversation

Rolling mills in the GCC operate in a market where raw material choices and logistics can change quickly, and that influences maintenance priorities. Fastmarkets described Saudi Arabia as having limited scrap availability relative to domestic requirements. It also reported four operational EAF-based steelmakers in Saudi Arabia, where three use around 80-85% DRI with the remainder ferrous scrap, while a fourth typically uses 15-20% DRI with most raw material as ferrous scrap. When input materials are disrupted, some GCC mills consider purchasing larger volumes of ferrous scrap and steel billet, pending logistical viability. This operating context creates pressure to protect uptime across bearings, hydraulics, and circulating systems because unplanned stops amplify procurement and delivery uncertainty.

The green steel transition is increasingly part of the GCC steel narrative, and it is also tied to lubricants through procurement standards and sustainability expectations. In Oman, Vale has been operating a 9Mtpa pelletizing plant since 2012, and it announced plans to transition the facility to 100% renewable energy by 2030 to reduce emissions. The IEEFA report also notes a 105-megawatt (MW) agreement with OQ Alternative Energy (OQAE) that will provide power for Vale’s planned Green Metallic Mega Hub in Duqm. The same report describes Oman as having an integrated steelmaking supply chain from global iron ore concentrate supply to electric arc furnaces for steelmaking. It also notes that, at present, all steel plants in Oman produce only long products, with plans underway to expand into flat products.

Beyond Oman, market signals and policy timelines matter. At MEIS, Jindal Steel’s CEO said the world’s DRI production is at 141 million tonnes, with 63 million tonnes coming from MENA, and cited natural gas around $4.8 in the Gulf compared with more than $10 in Europe. He also pointed to “close to 3,500 hours of sunshine,” wind resources, and national hydrogen policies as reasons the Middle East is well positioned for hydrogen-based steel production. Separately, Climate Energy Finance notes that EU CBAM enters into force on 1 January 2026. In lubricants, Kline describes GCC emissions-reduction targets and supplier responses such as expanding re-refined base oil capacity and launching eco-friendly formulations, tying regulation and sustainability goals to innovation in the lubricants sector.

What does “steel mill lubricants GCC” mean in practice for plant teams?

What reheating-furnace details matter most before rolling?

How DRI-heavy is Saudi EAF steelmaking, according to Fastmarkets?

What green transition milestones are cited for Oman’s steel value chain?

What is one policy timeline that can influence green steel positioning for MENA exporters?