For many plants, food grade lubricants GCC decisions are shifting from routine maintenance to compliance protection. Future Market Insights (FMI) frames food grade lubricants as a “structural pillar of food safety culture,” tied to avoiding chemical contamination and audit non-conformities. SkyQuest also links demand to rising consumption of processed foods and beverages and to diverse end-use sectors such as food, beverages, pharmaceuticals, and cosmetics.

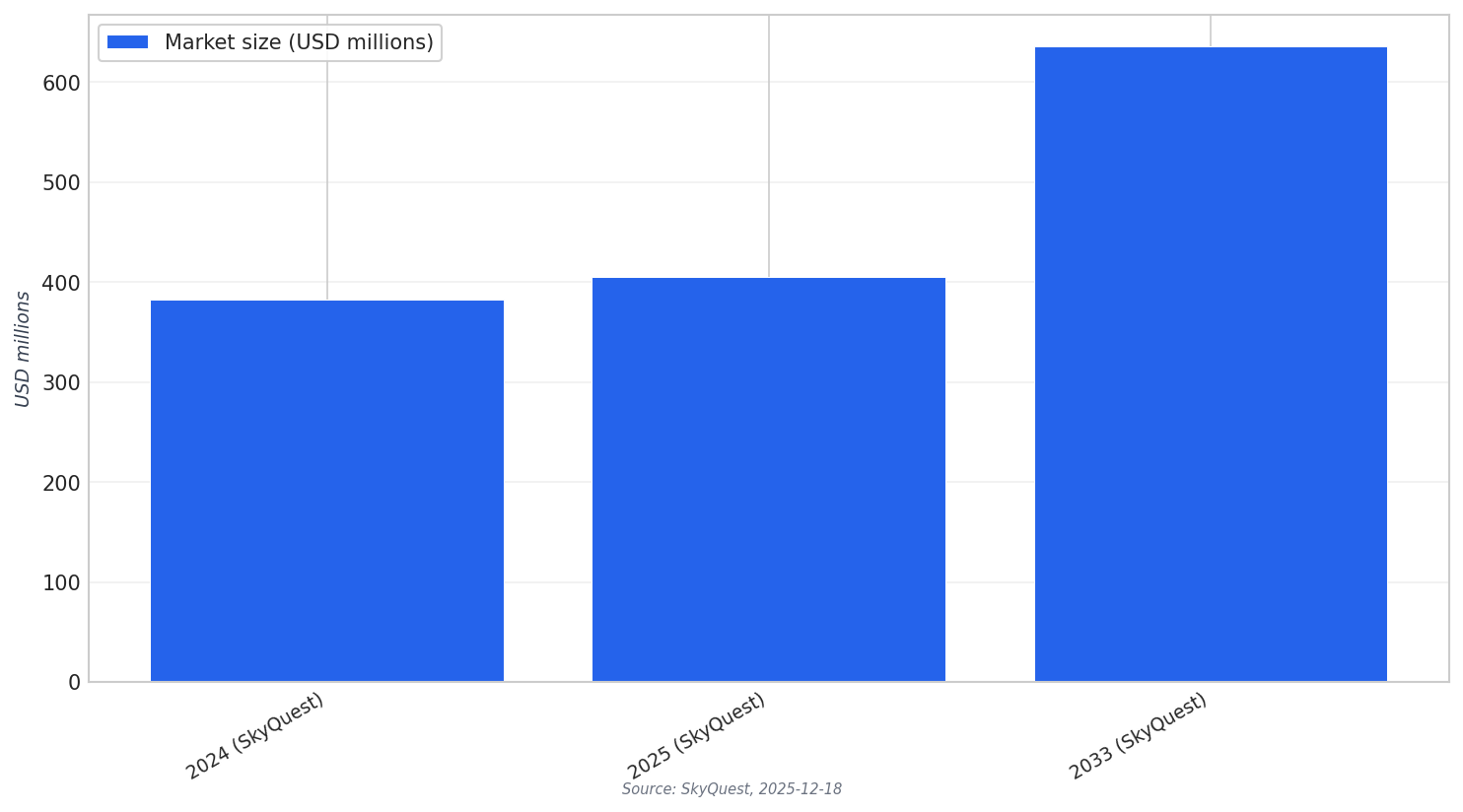

Global market projections underline the direction of travel. SkyQuest values the global food grade lubricants market at USD 382.86 million in 2024, growing to USD 405.07 million in 2025 and reaching USD 635.93 million by 2033. FMI reports a similar global baseline, valuing the market at USD 389.6 million in 2025, projecting USD 399.7 million in 2026 and USD 516.7 million by 2036. These figures are global, but they help contextualize why GCC operators focus on audit readiness and standardized practices rather than only price.

Compliance Is the Demand Engine: H1, Audits, and Traceability

FMI describes a “compliance gate” procurement model, driven by retailer mandates and Global Food Safety Initiative (GFSI) schemes. The result is broader adoption of NSF H1-registered lubricants across incidental-contact zones. FMI also warns that a non-H1 lubricant in a critical control point can trigger audit failures, line shutdowns, and reputational damage—pushing procurement toward documentation transparency and supplier traceability. STUFFF similarly emphasizes that food-grade lubricants support compliance with HACCP and GMP, and that using the wrong lubricant can contribute to failed audits or recalls.

Segment signals reinforce why standardization matters. FMI reports that H1 lubricants command more than 40% of market volume in 2026, reflecting “safety-first” operations that standardize on H1 fluids to reduce misapplication risk. FMI also states protein processing accounts for 35% of total demand in 2026. IndexBox adds that growth is underpinned by modernization of global food and beverage processing and rising hygiene and safety standards mandated by agencies such as the FDA, NSF, and EFSA, with buyers purchasing “risk mitigation and compliance assurance.”

Technology and format choices are also shaped by sanitation routines. IndexBox highlights a trend toward food grade dry film lubricants on components such as valve stems, pump seals, and filler heads, aiming to survive CIP cycles and reduce lubrication frequency and audit non-compliance risk. SkyQuest notes that bio-based lubricants derived from natural fats and oils are gaining traction as eco-friendly alternatives as regulatory measures and sustainable preferences increase. For GCC food processors scaling and formalizing operations, these themes point to a practical roadmap: prioritize certified products, traceable documentation, and lubrication programs aligned with audit expectations.

What is driving food grade lubricants GCC purchasing decisions toward compliance?

How large is the global food grade lubricants market, according to the sources?

Which product type leads demand in the sources?

Which end-use segment is highlighted as a major demand center?

Why do dry film lubricants show up in food safety discussions?