Interest in the bio-based lubricants Middle East market is rising for a practical reason: the overall lubricants pool is expanding, and decarbonisation pressure is spreading into “hidden” inputs like oils and additives. One regional forecast puts the Middle East lubricants market at 2.94 billion liters in 2025 and projects it will reach 3.31 billion liters by 2030. Another market view sizes the region at 2.87 billion liters in 2025, with growth from 2.95 billion liters in 2026 to 3.36 billion liters by 2031. Across sources, the direction is consistent: steady volume growth creates room for new formulations, including bio-based options.

In parallel, product technology is changing how lubricants are used. Modern additives have enabled lubricant change intervals to increase from 5,000 km in legacy vehicles to upwards of 30,000 km in modern engines. KPMG Middle East’s viewpoint in regional trade media adds that bio-based or biomass-balanced additives can reduce emissions linked to additive manufacture while enhancing overall oil performance. This matters commercially because value can shift from “liters sold” to “performance delivered,” supported by tools like digital monitoring that reduce waste during use.

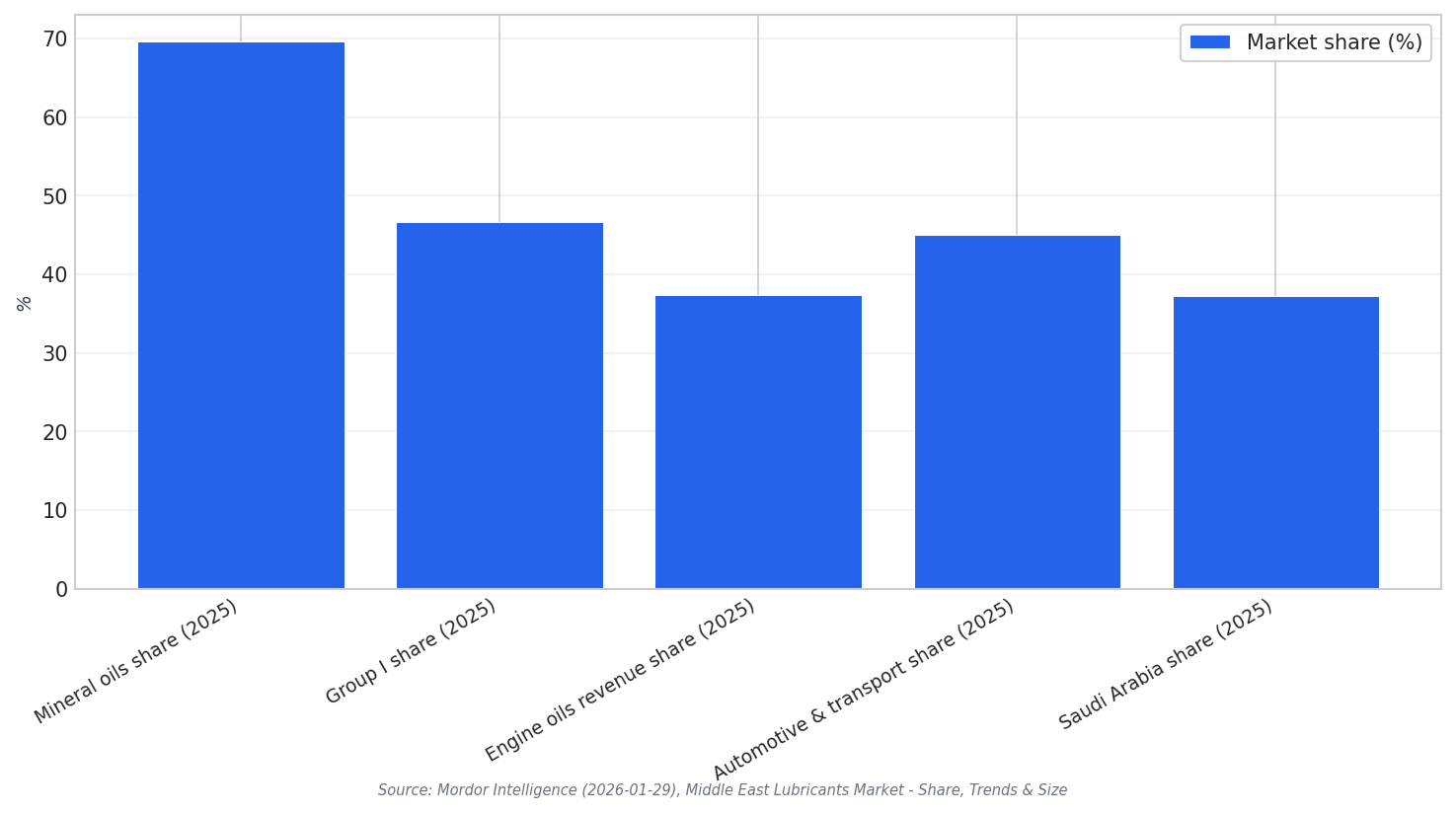

Bio-based options also have an infrastructure advantage. Reported commentary states these bio-based oils can perform similarly to fossil-based ones, have a lower carbon footprint, and can be processed using existing infrastructure. That combination can help adoption in heavy industrial settings that cannot easily change equipment or supply chains. It also aligns with a market where mineral oils still dominate: mineral oils held a 69.58% share of the Middle East lubricants market in 2025, while bio-based lubricants are forecast to grow at a 3.12% CAGR through 2031.

Where Demand Is Building Beyond the “Green” Narrative

Demand signals are strongest in large consuming sectors. Saudi Arabia led with 37.21% of Middle East lubricants market share in 2025. The automotive and other transportation end-user category commanded 45.02% of the market in 2025. Another source notes Saudi Arabia projects internal combustion engine vehicles to remain dominant for the next 15–20 years, supporting baseline lubricant demand even as formulations evolve. Industrial expansion adds further pull. One Middle East-focused update cites Saudi allocation of USD 293 billion toward power and renewable energy projects, crude steel output at 9.9 million metric tons in 2023, and USD 12 billion in new steel projects—each tied to machinery, maintenance, and process lubrication needs.

Opportunities also appear in niche but high-value segments. An offshore-focused market note links growth to expanding offshore oil and gas activity and states that bio-based lubricants are expected to capture 25% of that market “by future.” The same source references projected investments of $20 billion connected to offshore expansion. Meanwhile, within the broader mix, transmission and hydraulic fluids are advancing at a 3.01% CAGR (2026–2031), and power generation is the fastest-growing end-user at a 3.09% CAGR to 2031. For suppliers, these categories can be a practical wedge for bio-based or biomass-balanced additive strategies where performance, monitoring, and longer life are valued.

What is driving the bio-based lubricants Middle East opportunity?

How fast are bio-based lubricants expected to grow in the Middle East market mix?

Which end-user segments matter most for lubricant volumes in the region?

What performance trend supports lower-emission lubricant strategies?

Is there evidence of bio-based momentum in offshore applications?